This article is a part of your HHCN+ Membership

UnitedHealth Group (NYSE: UNH) and Amedisys Inc. (Nasdaq: AMED) announced combination plans last June, under which home health giant Amedisys would become part of Optum.

Amedisys had previously entered into an agreement to merge with infusion therapy company Option Care Health (Nasdaq: OPCH), but UnitedHealth Group’s offer, scale and complementary clinical capabilities were effectively too good to pass up. As with any deal of this magnitude, however, there are complications.

Perhaps the biggest hurdle in the way of Amedisys and UnitedHealth Group successfully executing their transaction – valued at about $3.3 billion – is the government’s concern around market competition. As recently as March, reports circulated claiming the U.S. Department of Justice was still considering an antitrust case blocking the sale of Amedisys.

Others, including Sen. Elizabeth Warren (D-Mass.), continue to scrutinize UnitedHealth Group for its M&A activity more broadly. Also in March, Warren released a statement slamming Steward Health Care’s plan to sell its physician group to Optum.

“Optum, a UnitedHealth Group subsidiary, is already the largest employer of physicians in the country – controlling over 10% of American doctors – which means this deal raises significant antitrust concerns in Massachusetts and nationally,” the senator said.

In the case of Amedisys, regulators are likely spending more time evaluating industry-competition ramifications because UnitedHealth Group and Optum acquired one of Amedisys’ largest competitors, LHC Group, at the beginning of 2023. A combined Amedisys-LHC Group enterprise would mean Optum owns a sizable chunk of the historically fragmented home health market.

To pave the way for its sale, I expect the Baton Rouge, Louisiana-based Amedisys to explore a multifaceted divestment strategy, which could include selling off parts of its core home health business and other measures.

I examine what divestiture could look like – and outline some key questions Amedisys will likely need to consider – as part of this week’s exclusive, members-only HHCN+ Update.

The core home health business

Divestment is something that the Amedisys leadership team is already weighing, according to Jefferies. In a recent note, analysts from the investment banking and financial services company wrote that they believe Amedisys management is “working on divestitures” that they view as “necessary” to get regulatory approval of their deal.

Jefferies analysts also said in their note they expect the Amedisys-Optum deal to be completed in the next few months.

Deciding how to break up the core home health business would be the most important aspect of a potential divestment strategy.

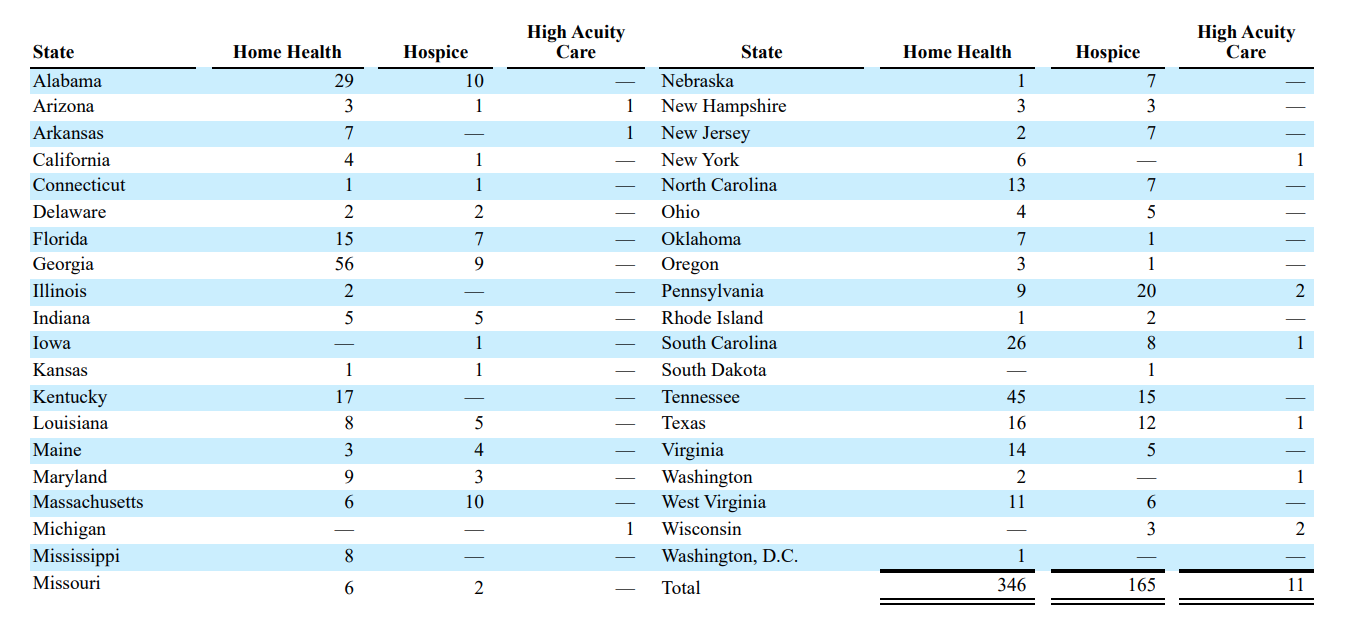

As of February, Amedisys provided home health, hospice and higher-acuity care services across 521 care centers in 37 states, plus the District of Columbia. That network included more than 200 home health locations in difficult-to-enter states requiring certificates of need (CONs), permits of approval (POAs) and/or facility need reviews (FNRs).

Specifically, according to its annual report filed with the Securities and Exchange Commission (SEC), Amedisys had 233 home health centers in 14 such states and Washington, D.C., with especially strong density (20+ locations) in Alabama, Georgia, South Carolina and Tennessee.

Overall, Amedisys at the end of last year had 346 Medicare-certified home health care centers in nearly three dozen states, according to its annual report.

Geography will likely be a deciding factor in any divestment strategy around the core home health business, I expect. If regulators are concerned about a combined Amedisys-LHC Group under Optum having too much market share, Amedisys could look to offload centers where there’s ample overlap with legacy LHC Group locations.

That’s easier said than done, though, with Amedisys and LHC Group having similar footprints.

As of March 2022, LHC Group had 557 home health locations, with density in many of the same states as Amedisys, such as Alabama and Tennessee, among others.

Because the footprints are comparable, Amedisys may need to take a center-by-center approach to divestment while simultaneously considering factors beyond geography. One possibility could be examining payer mix or a market’s Medicare Advantage (MA) penetration as part of a divestment strategy.

Despite most Medicare beneficiaries having access to plans operated by several different insurance firms, MA enrollment in 2023 was concentrated in plans operated by UnitedHealthcare and Humana (NYSE: HUM), according to Kaiser Family Foundation data. Those two entities alone accounted for nearly half of all 2023 MA enrollment.

I could see a scenario where Amedisys’ home health locations with higher levels of MA business being prioritized.

Amedisys has been successful in growing its non-fee-for-service Medicare revenue over the years.

For full-year 2023, the Amedisys home health business had a net service revenue of about $1.4 billion. Medicare revenue on the year came in at $874.2 million, while non-Medicare revenue totaled $529.4 million.

If Amedisys does sell off parts of its core home health business, it will likely have plenty of suitors. Along with Option Care and Optum, in fact, Amedisys attracted M&A interest from other payer-type buyers last year.

Carving out hospice

Identifying divestiture opportunities in its home health business is Step 1 for Amedisys. Once the Amedisys-UnitedHealth Group transaction closes, Step 2 will be figuring out what to do with Amedisys’ hospice line.

Pairing LHC Group and Amedisys under Optum wouldn’t just give UnitedHealth Group a large portion of the home health market. It also would make Optum a hospice leader – and I question just how valuable that is for UnitedHealth Group.

As of December 2023, Amedisys had 165 Medicare-certified hospice care centers in over 30 states. For full-year 2023, the hospice business line brought in $798.8 million in net services revenue.

Expanding into hospice had been a major focus for Amedisys heading into the Patient-Driven Groupings Model (PDGM) implementation Year 1, with its industry-shaping end-of-life care deals including its $340 million purchase of Compassionate Care Hospice in 2018.

“We wanted to go out and balance any ill effects there may be — or may not be — with PDGM,” Amedisys Chairman and former CEO Paul Kusserow told HHCN at the time. “We wanted to bulk up on hospice, which has a very near-term, rosy regulatory future, so we believe this should offset any of the PDGM chop that could occur.”

Meanwhile, LHC Group has also worked to methodically grow its hospice arm, seeking to co-locate or even tri-locate its home health, hospice and personal care services lines.

As of December 2022, LHC Group operated 159 hospice locations, of which 96 were wholly-owned and 61 majority-owned through equity joint ventures. Two were under license-lease arrangements.

LHC Group’s hospice net services revenue for full-year 2022 was about $407.5 million, according to its last annual report filed with the SEC.

Since LHC Group became part of Optum, I’ve wondered exactly how hospice fits. Home health has been shifting toward MA and value-based care, but hospice is still predominantly paid for by traditional Medicare.

That isn’t going to change any time soon, either, with the U.S. Centers for Medicare & Medicaid Services revealing in March that the agency will end the hospice component of the Value-Based Insurance Design (VBID) model at the end of the year. Effectively, hospice is being carved back out of MA again.

Hospice is an incredibly valuable service, but there’s not the same degree of synergy with the broader UnitedHealth Group, I believe.

So what’s going to happen? Well, I can see UnitedHealth Group eventually taking a page out of the Humana playbook. An Amedisys-LHC Group hospice enterprise would be extremely valuable, and UnitedHealth Group could sell a majority stake in that combined business similar to what Humana did with the legacy Kindred/Curo platform.

Humana completed a $2.8 billion sale of Kindred at Home’s hospice and personal care segments, divesting a 60% stake, to the private equity firm Clayton, Dubilier & Rice in August 2022.

“Humana will continue to support the long-term success of these operations through our minority ownership and ongoing strategic partnership,” Humana CFO Susan Diamond said at the time. “Hospice and palliative services play an important role in the full continuum of care, and we are confident that this new standalone company will continue to provide patients and their families with the resources and high-quality care they need.”

Contessa questions

Contessa is Amedisys’ higher-acuity care engine, acquired for $250 million in 2021. Contessa was once a standalone business – and there’s always the chance it could be again in a post-Optum future.

But I see Optum and Amedisys wanting to keep Contessa and all of its higher-acuity care capabilities, which include hospital-level care in the home, home-based palliative care and its SNF-level care in the home.

Strategically, Contessa’s higher-acuity care know-how would amplify some of Optum’s other care delivery assets. It’s important to note that, in 2021, Optum also purchased Landmark, and, in 2023, it acquired Prospero Health.

Contessa has largely found success via its joint venture strategy, however. Optum ownership could complicate existing JV arrangements, or make some potential health system or payer partners hesitant.

It has happened before

This week’s HHCN+ Update is purely an exercise on how Amedisys might think about divestment, if that’s something it sees as beneficial in working toward a finalized Optum deal.

In this exercise, though, it’s useful to remember that Amedisys does have a recent track record of strategically separating parts of the business. The company just took that very measure with its personal care business, which at the time of divestment included 13 care centers in three states.