This article is a part of your HHCN+ Membership

Transaction volume for home health, home care and other in-home care businesses dipped in 2023, with inflation, higher interest rates and global unrest contributing to the downturn.

Many home-based care stakeholders anticipated M&A to rebound in 2024, however, thanks to increased loan activity in January, greater buyer-seller consensus and private equity’s record-high levels of “mature” dry powder.

With 2024’s first quarter in the rear-view mirror, the home-based care dealmaking outlook still looks to be a bit of a question mark.

“Things can change in a short amount of time and have a profound impact on the marketplace,” Mark Kulik, senior managing director at M&A advisory firm The Braff Group, said last week at the Home Health Care News Capital + Strategy Conference in Washington, D.C.

While it may be too soon to call 2024 a bull or bear market for M&A, I am starting to notice a few interesting trends, many of which surfaced at the Capital + Strategy Conference. Some of those trends include:

– The 2024 forecast for home-based care transaction volume is cloudier than just a few weeks ago, with the Federal Reserve seemingly more wary of interest-rate cuts.

– Buyers and sellers are increasingly aligned, though some sellers are still holding out for 2020- and 2021-level valuations. Some are bridging the buyer-seller gap with earnout structures.

– Investors are more optimistic about the current in-home care staffing environment, with many seeing labor pressures alleviating compared to the historically challenging stretch coming out of the public health emergency.

– While some buyers remain focused on a particular care lane, others continue to pursue continuum and diversification strategies.

– More acquirers are touting their proprietary M&A strategies. Unsurprisingly, the No. 1 business characteristic buyers are targeting: quality.

In this week’s exclusive, members-only HHCN+ Update, I share some of my biggest takeaways from our conference.

Monetary-policy whiplash

Home-based care transaction volume plummeted in 2023, mirroring the broader global health care dealmaking trend. Some of the dip was a return to mean, with 2021 experiencing record M&A activity and 2022’s action robust as well.

The cost of capital was arguably the primary hindrance to dealmaking, with the Federal Reserve attempting to control inflation via its most impactful economic tool: interest-rate policy. From March 2022 through July 2023, the U.S. central bank has raised the fed funds rate by more than five percentage points, making no fewer than 11 individual hikes.

“This is akin to the Fed jamming the brakes on the monetary policy to help slow down the economy because inflation was occurring,” Kulik explained at the Capital + Strategy Conference.

Going into 2024, the Federal Reserve had signaled intentions to cut rates, with relief possible coming in the second or third quarter. That gave home-based care buyers and sellers reason for optimism.

That excitement has dissipated over the last week. As recently as Tuesday, officials explained that inflation remains more stubborn than they anticipated, meaning interest rate rates will likely stay high.

“Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us,” Federal Reserve Chair Jerome Powell told a forum in Washington.

At the Capital + Strategy Conference, it felt like the discussions around the broader U.S. economic climate were giving buyers and sellers whiplash. In turn, I see buyers and investors operating with the same conservative mentality on display in 2023.

Still, one factor that could mitigate that is the ample dry powder that private investors are sitting on, according to Bain & Company data, which Kulik cited during a presentation at our event. With about 26% of global buyout dry powder now four years or older, some are feeling heightened urgency to get deals done.

“Investors gave them money to invest in buy, and they didn’t deploy it,” Kulik explained. “And there’s pressure on private equity to deploy that cash because investors want a return on their money. They don’t want to just let it park in a savings account in a bank.”

Narrowing the gap

Home-based care sellers in 2023 valued their businesses at 2020 and 2021 levels, when valuations for home health, home care and hospice providers were extremely high. There is still a gap between today’s more conservative buyers and hopeful sellers, but it’s beginning to shrink, multiple executives said at the Capital + Strategy Conference.

“I do feel like that gap between expectation and what buyers are willing to pay has come closer – considerably,” Cameron Cordts, corporate development manager for PurposeCare, said at the event.

Backed by Lorient Capital, PurposeCare is a home health and home care provider focused on building density in the Midwest. The provider has announced several acquisitions over the past couple years, including three at the start of 2024.

In some cases, the gap is closing because of segment-specific factors, such as fee-for-service Medicare rates or the looming 80/20 rule in Medicaid. These and similar industry-specific challenges become the final straw for some prospective sellers.

In others, sellers have finally come to realize that buyers aren’t willing to pay 2020 and 2021 terms. Having been on the market for an extended period, these sellers have now accepted their fate.

“It is starting to shift a little bit,” Mike Trigilio, CEO of HouseWorks, said at the Capital + Strategy Conference. “There are some [sellers] coming on the market in the last few months that probably waited through 2023, that weren’t around last year. We’re seeing tons of opportunity.”

The InTandem Capital-backed HouseWorks has been one of the most acquisitive home-based care companies since late 2021, with its purchases including the personal care division of Amedisys (Nasdaq: AMED), Elite Home Health Care and several others. Service and payer diversification have been two of the company’s core M&A pillars.

Some buyers are taking it upon themselves to bridge the divide between acquirers and sellers. One way to do so is through deal earnout structures.

Care Advantage – the home-based care company backed by Searchlight Capital – has been successful with this approach, according to Jaron Clay, the company’s VP of integrations. Care Advantage has completed close to two dozen transactions since 2018, with Nova Home Health Care one of its more recent acquisitions.

Four of its last five deals have included earnout structures, Clay noted.

“We’ve pushed a lot more toward doing earnout structures on a lot of our deals,” he said at the event. “That’s a way for us to have the certainty that we want around this business not falling off the cliff when the owner/operator leaves. But it also is a way for us to actually give that person more money – maybe not all on Day 1. They’re getting some of it 12 months or 24 months down the road.”

I do feel like that gap between expectation and what buyers are willing to pay has come closer – considerably.”

– Cameron Cordts, corporate development manager, PurposeCare

Staffing success paying off

Another frequent comment I heard during the Capital + Strategy Conference: Home-based care staffing challenges are leveling off.

“Across our portfolio, we’ve seen improvements,” Scott Plumridge, managing partner at the Halifax Group, said at the conference. “I think our operators would characterize it as easier, but still not easy.”

The Halifax Group in September acquired the worldwide home care division of Sodexo, including the Comfort Keepers brand.

Contextually, home health, home care and hospice agencies have long faced a staffing deficit. Demand for aging-in-place and end-of-life care services is increasing faster than supply – and that will remain true as baby boomers transition into their 65+ era.

But the overall labor market is improving, and home-based care providers are also getting better at attracting and retaining talent.

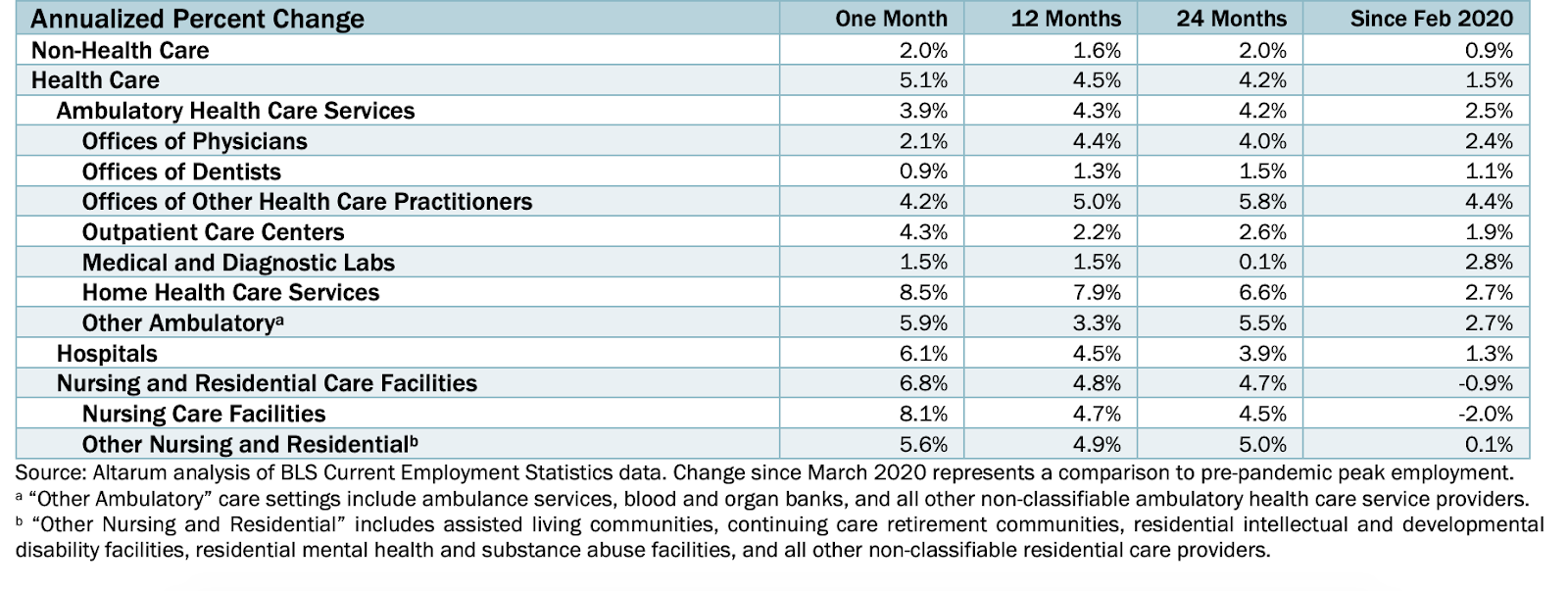

Altarum’s most recent Health Sector Economic Indicators brief supports this notion. In March, the seasonally adjusted change in employment was 8.5% for home health care services, up from the 24-month mark of 6.6%.

That’s among the strongest employment gains in all of health care.

Kenneth Hammond, the chief investment officer for Kaltroco, echoed Plumridge’s comments.

“2022 was the moment of the most intense [staffing] pressure,” said Hammond, whose organization is the investment partner of New Day Healthcare. “And certainly, the situation has gotten better.”

While overall labor-market improvement is helping the staffing situation stabilize, the provider-driven efforts making a dent include sign-on bonuses and other enhanced benefits, smarter scheduling, the automation of non-care functions and more.

The continuum of care

Although there are certainly still buyers that prefer to focus on one core service, forward-looking in-home care operators continue to build out a complete continuum of care. I view this strategy as a long-term trend propelled by value-based care and the consumerization of health care.

New Day is among the home-based care companies that consider the care continuum in M&A opportunities.

“We are open minded to good businesses across the board, from skilled home health, to Medicaid [personal care], to hospice,” Hammond said. “From a platform standpoint, as we enter new states, we like businesses that have begun to solve that [continuum] problem, right? We look for companies that have at least two of the three legs of the stool, so that we can deploy organic growth to go pursue that continuum strategy that we bring data into.”

Having a continuum of home-based care service lines allows providers to maintain longitudinal relationships with clients. An older adult may turn to non-medical home care for activities of daily living (ADL) support, but that could eventually turn into a home health or hospice relationship.

Payers also appreciate providers with diverse service offerings.

“Our goal is to create a continuum of care, primarily leading with home care on the non-skilled side, then supplementing with home health care,” Cordts said.

At the Capital + Strategy Conference, it was evident to me that continuum and diversification strategies included far more than just home care, home health and hospice. Companies such as Care Advantage, for instance, are working to build care continuums for specific populations.

“We’ve really been focusing on being disciplined around what we’re very, very good at, which is personal care,” Clay said. “How can we do some of those things that aren’t a hop, skip and jump away from that, but a step away from that?”

An example: Care Advantage has acquired home care providers that specialize in certain cultural demographics. This creates strong provider-client relationships while also differentiating Care Advantage in those markets.

“That has proven to be a very sticky business, a very profitable business for us,” Clay continued. “But most importantly, a really rewarding one.”

We’ve really been focusing on being disciplined around what we’re very, very good at, which is personal care. How can we do some of those things that aren’t a hop, skip and jump away from that, but a step away from that?

– Jaron Clay, VP of integrations, Care Advantage

Active acquirers tout DIY M&A

The M&A process can be a taxing one, so it’s not a shock that many buyers and sellers enlist the help of an expert dealmaking facilitator. That’s not always the case, though, with even some of the largest in-home care providers in the country previously touting their internal M&A efforts.

While at the helm as the CEO of Amedisys, Paul Kusserow was always keen on highlighting the provider’s proprietary M&A process.

“We built our own proprietary M&A function that can find these assets,” Kusserow told me in 2018. “We bought [Compassionate Care Hospice] way below what the market has been trading at for these assets. Hopefully this will start a trend where people are not overpaying for these things because some of the prices that have been out there are ridiculous.”

At the Capital + Strategy Conference, it felt like more providers were making similar remarks.

At HouseWorks, a majority of the company’s previous 10 deals were sourced internally, Trigilio said. Quality is usually the starting point in those processes, he added.

“The key ingredients are compliance and quality,” he said. ”The care delivery is always at the beginning of all these transactions.”

The same holds true for PurposeCare, according to Cordts.

“They’re not as competitive, but typically involve maybe a little bit more time for my team, and myself, bringing that seller along in the process,” he said. “That’s been the majority of our growth in the last year or so – harvesting those proprietary leads and educating sellers on where the market is at, and what those expectations can lead to.”

Companies featured in this article:

Care Advantage, HouseWorks, Kaltroco, Lorient Capital, PurposeCare, The Braff Group, The Halifax Group