This article is a part of your HHCN+ Membership

It’s no secret that private equity is shaping the present and future of home-based care in the United States.

It appears to me that in-home care is also rubbing off on PE, however, with multiple examples of the idea coming this week.

Generally speaking, private investment groups can come in all shapes and sizes. For the most part, though, PE firms invest in companies with the belief they can unlock additional value through their resources, connections and expertise, then cash out after that mission has been accomplished.

“At some point, private equity buys,” Jim Moskal, a partner at M&A and debt advisory firm Livingstone Partners, told me in April while predicting a rise in home care franchiser dealmaking. “At some point, private equity sells.”

In the past, PE exits in home health and home care have been pretty straightforward: One firm simply offloads its asset to another firm. But increasingly, I’ve noticed PE investors hanging around by retaining a sizable stake in the home-based care organizations they’re selling.

That’s exactly what Wellspring Capital Management did last fall, for example, when it sold the bulk of Chicago-based Help at Home to the PE duo of Centerbridge Partners and The Vistria Group. Financial terms of that transaction were not disclosed, but PE Hub reported the deal was around $1.4 billion.

Now, Centerbridge and Vistria are reportedly looking to do something similar with Sevita, the national provider of community-based health care and support services that recently rebranded from Civitas. On Wednesday, rumors surfaced that the two PE powerhouses are hoping to sell a minority stake in Sevita, with the sales process expected to last another two to three weeks.

The Boston-based Sevita delivers home- and community-based care to roughly 50,000 individuals across 40 states. Its offerings range from in-home care and adult day support for seniors, to family behavioral health services and children’s autism services.

Sevita actually added to its service mix on Wednesday, announcing the acquisition of multiple Help at Home supportive living and day center services.

“We are proud to welcome care teams and individuals served through Help at Home’s supportive living, shared living, periodic and day center services into the Sevita continuum of care,” Sevita CEO William McKinney said in a press release announcing the news. “Dynamic relationships between caregivers and individuals are the bedrock of our work. Help at Home’s exceptional caregivers will help Sevita continue to offer quality care for the people we serve.”

PE firms aren’t just holding on to portions of their home-based care investments longer. They’re also frequently becoming repeat investors in the space, which, I believe, reflects the strength of the market.

Wellspring, again, is the perfect illustration of that. On Monday, the former majority owner of Help at Home struck a deal for Caring Brands International, the parent company of Sunrise, Florida-based Interim HealthCare.

“We have been strong advocates of high-quality home-based care providers that enable seniors, individuals with medically complex care needs and others with disabilities to live independently in their homes,” Naishadh Lalwani, a partner at Wellspring, said in a statement.

Uninvested cash

Home-based care operators need to be aware of the changing nature of PE investment because it’s not going to slow down anytime soon.

As of the end of August, the top 25 private equity firms were sitting on $509.8 billion in uninvested cash, according to data from S&P Global Market Intelligence and Preqin. Combined, those firms held over 22% of the global dry powder.

While firms can take their money and go anywhere, more and more are turning to health care, particularly the parts of the sector seeing significant investment in next-generation models. And today, you can’t say “the future of health care” without mentioning “the home” in the very next breath.

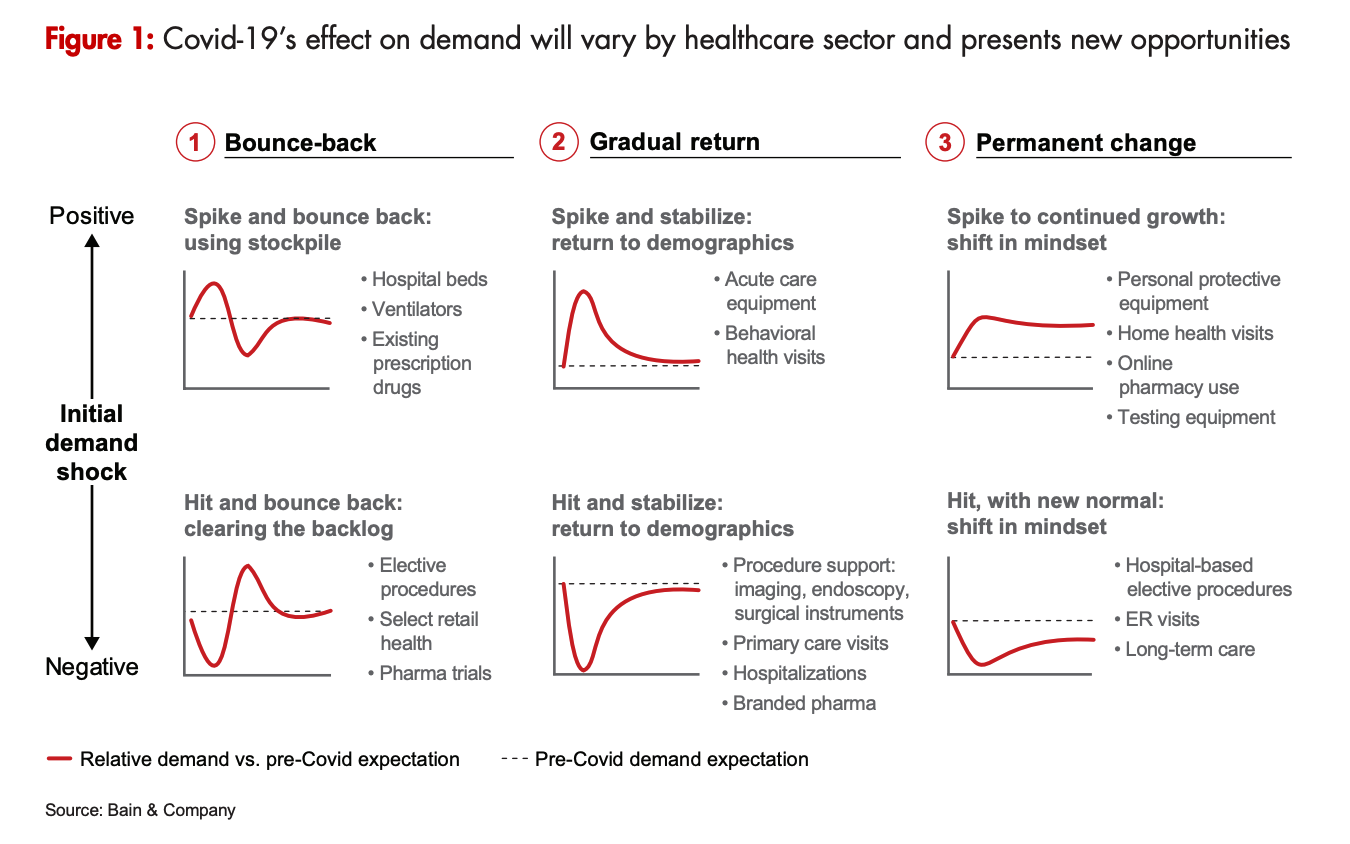

“While people used to view home health visits, virtual pharmacy and telemedicine practices as niche channels for care, the pandemic forced many people to try virtual options,” Bain & Company wrote in its 2021 report on global health care private equity and M&A activity. “Given the greater willingness to use emerging forms of health care, we expect demand for these types of alternative channels to increase.”

Additionally, PE firms are likely to continue targeting home-based care because of the highly fragmented nature of the home health and home care industries. Often, private investors see health care provider segments with room for buy-and-build strategies as prime hunting grounds.

Coltala Holdings and Trive Capital are pursuing such a strategy with Choice Health at Home. Backed by PE firm Dorilton Capital, Traditions Health is another buy-and-build home health play to keep an eye on.

“Home health care had become a more important channel even before the pandemic,” the Bain & Company report continued. “This trend stemmed not only from patients becoming less reliant on visiting higher-acuity sites, but also on favorable reimbursement changes, especially in the US. Now there is an opportunity for enhanced levels of care at home, as well as systems that support patient movement between care settings.”

What this all means

Often, when a PE buyer invests in a company, it has an exit window of between four and seven years.

The fact that some firms are holding on to pieces of home-based care assets even after that window expires suggests they still see ample room on the runway before a true takeoff.

That view makes sense, considering the U.S. hasn’t come close to feeling the full impact of the “silver tsunami,” or the wave of baby boomers reaching their Medicare-eligible years.

Currently, over 54 million people living in the U.S. — or about 16% of the nation’s population — are over the age of 65, the most recent census shows. By 2030, that figure will rise to about 74 million, with the number of people over the age of 85 growing at an even faster rate.

The demographic shift is largely why the Biden administration wants to include additional funding for senior care in the Democrats’ social spending package, which, as of Thursday, is rumored to be around $1.75 trillion.

Similarly, the fact that PE players like Wellspring and others circle back to home-based care shows the immediate strength of the market, even when it comes to smaller, mom-and-pop businesses.

“I’m selling transactions at valuations that would have been unheard of two years ago,” Rich Tinsley, president and CEO of M&A advisory firm Stoneridge Partners, told me during a conversation at FUTURE.

Here’s one last thought on PE and home-based care before I wrap up: Since COVID-19 began, private investors have been highly scrutinized for gutting nursing homes to maximize profits, leaving residents in incredibly vulnerable positions amid the pandemic.

Sen. Elizabeth Warren, a Democrat from Massachusetts, just recently took aim at PE while chairing a Senate hearing on the financial sector.

“We’re seeing it all around the health care sector,” Warren said. “Once private equity starts buying local businesses, communities too often turn out to be the losers.”

If private equity relationships are evolving to become more long term in home-based care, that could help deflect some of that heat. Additionally, the ownership continuity may also benefit providers themselves.

Companies featured in this article:

Bain & Company, Choice Health at Home, Coltala Holdings, Dorilton Capital Advisors LLC, Livingstone Partners, Stoneridge Partners, Traditions Health, Trive Capital