In addition to high interest rates, there’s another factor slowing down health care and post-acute care M&A, according to a new report.

Released last week, Pitchbook’s Q4 health care services report shines a light on the Biden administration’s antitrust and private equity stances, and how those may be affecting dealmaking.

For instance, the Humana Inc. (NYSE: HUM) and Cigna Group (NYSE: CI) combination rumor ended late last year with the insinuation that the two massive payers couldn’t agree to a price tag. But Pitchbook – and its lead health care analyst, Rebecca Springer – believe that a heightened antitrust focus from the president’s administration also could have played a role.

In late November, initial reports came out regarding Humana-Cigna conversations. By Dec. 11, those conversations had ended.

“Cigna and Humana call off merger talks, which were first reported in November,” the Pitchbook report noted. “Antitrust opposition is believed to have contributed to the deal’s demise. Many payers are under pressure due to rising utilization, slowing growth, and changes to the Medicare Advantage (MA) program.”

UnitedHealth Group (NYSE: UNH), and its subsidiary Optum, are in the process of navigating this more complex regulatory landscape as well.

A prolific acquirer, Optum is beginning to meet more pushback on its acquisitions. Its deal for the home health and hospice provider Amedisys (Nasdaq: AMED) has already received scrutiny from lawmakers. If it acquired Amedisys, Optum would own about 10% of the home health market, having already acquired LHC Group.

At the same time, its planned takeover of the Corvallis Clinic in Oregon is also receiving significant pushback.

Elsewhere, on Dec. 7, the Biden administration released a fact sheet condemning certain PE activity in the health care space, including in home-based care.

“Private-equity ownership in the health care industry has ballooned, with approximately $750 billion in deals between 2010 and 2020 – in sectors including, but not limited to, physician practices, nursing homes, hospices, home care, autism treatment and travel nursing,” the fact sheet read. “Too often, aggressive profiteering by private equity-owned practices can lead to higher patient costs and lower quality care.”

Though interest rates likely remain the no. 1 deterrent to activity, this dynamic also appears to be playing a role.

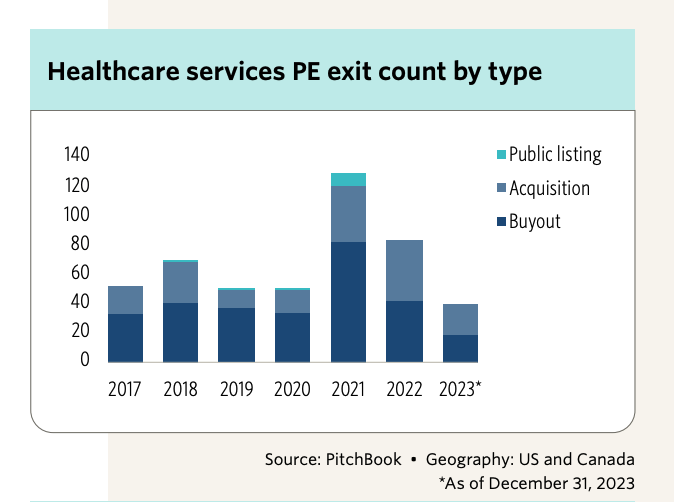

While there are more PE-backed health care companies than ever, new investments and new exits have waned over the past few years.

“The key effect of the Biden administration’s scrutiny of PE in healthcare is not direct antitrust risk, but headline risk,” Springer wrote. “We have been struck by the sudden change in tone among investors on this topic. While the interest-rate environment remains the most important driver of the pace of dealmaking, we also believe sponsors will be somewhat more cautious in 2024 about entering any provider categories that primarily serve vulnerable populations, including home-based care, post-acute care, high-acuity behavioral health, intellectual & developmental disabilities (IDD) care and autism treatment.”